.avif)

.png)

.png)

.avif)

Group insurance has become one of the most important employee benefits for companies in India. As healthcare costs rise and workplace risks evolve, employers are increasingly turning to structured insurance plans to protect their teams while improving retention and long-term wellbeing.

In simple terms, group insurance refers to insurance coverage provided by an organisation to a group of people — usually employees — under a single master policy. Instead of individuals buying policies separately, the employer purchases coverage that extends to the entire workforce, often at more affordable rates and with broader benefits.

This guide explains what group insurance means in the Indian context, the different types of policies available, and how companies decide which coverage makes sense for their teams.

What is group insurance?

Group insurance is a single policy that covers multiple members under one plan. In most cases, the employer acts as the policyholder while employees are the insured members.

Unlike individual policies, underwriting for group insurance focuses on the organisation rather than each employee’s medical history. This allows companies to offer broader coverage, fewer exclusions, and easier onboarding for employees.

Key characteristics of group insurance include:

- Coverage offered as an employee benefit

- Standardised benefits across the organisation

- Simplified enrollment and renewal processes

- Lower premiums due to risk pooling

In India, group insurance is commonly structured around health coverage, life protection, and accident benefits. Many organisations combine multiple policies to build a comprehensive employee protection strategy.

Why group insurance is becoming essential for Indian employers

The demand for structured employee benefits has grown significantly over the last decade. Rising medical inflation, increased workforce expectations, and a competitive talent market have made insurance a core part of compensation strategy.

Several trends are driving adoption:

Healthcare costs are rising faster than salary growth

Hospitalisation expenses continue to increase year on year, making employer-provided coverage a practical safety net for employees who may not have personal insurance.

Employees expect protection beyond salary

Younger workforces now evaluate companies based on benefits as much as pay. Group insurance signals stability and long-term care from the employer.

Compliance and risk management are evolving

Many organisations use group policies to reduce financial exposure and create structured frameworks for employee safety and welfare.

Types of group insurance offered by companies

Most organisations structure their benefits around three core insurance categories. Each serves a different purpose, and together they create a more balanced protection framework.

Group health insurance

Group health insurance covers medical expenses such as hospitalisation, pre- and post-hospitalisation care, daycare procedures, and sometimes outpatient consultations.

For many employees in India, this is their primary source of health coverage. Employers typically choose sum insured slabs based on team size, industry risks, and budget.

Common features include:

- Cashless treatment across network hospitals

- Coverage for dependents such as spouse, children, and parents

- Preventive health checkups and wellness benefits

- Maternity coverage in some plans

From an employer perspective, group health insurance helps reduce absenteeism and provides financial protection during medical emergencies.

Group term life insurance

Group term life insurance provides financial support to an employee’s family in case of death during the policy term. Unlike investment-linked plans, term insurance focuses purely on protection.

Coverage amounts are often linked to salary multiples or fixed slabs defined by the employer. This type of policy plays an important role in long-term financial security for employees’ families.

Benefits typically include:

- Lump sum payout to nominees

- Affordable premiums due to group pricing

- No individual medical underwriting in many cases

Organisations often use group term life insurance to create a baseline safety net across the workforce.

Group personal accident insurance

Group personal accident insurance offers protection against accidental injuries, disability, or death caused by unforeseen incidents.

While health insurance covers treatment costs, personal accident policies provide additional financial compensation for events that impact earning capacity.

Coverage may include:

- Accidental death benefits

- Permanent or partial disability payouts

- Temporary total disability compensation

- Education or rehabilitation benefits in some plans

Industries with travel-heavy roles or operational risk exposure often prioritise this coverage alongside health insurance.

How group insurance works for employers

Understanding the structure of group insurance helps companies make better decisions about coverage design.

Policy ownership

The employer purchases and manages the policy, while employees become members of the group. Premiums may be fully employer-paid or shared with employees depending on the benefit structure.

Risk pooling

Insurers evaluate risk at the group level rather than individually. Larger employee pools often lead to more stable pricing and fewer restrictions.

Customisation options

Employers can define:

- Sum insured levels

- Dependent coverage

- Add-ons such as maternity or wellness benefits

- Policy extensions for parents or partners

This flexibility allows organisations to tailor coverage based on workforce demographics.

Benefits of group insurance for employees

Group insurance goes beyond financial reimbursement during emergencies. For many employees in India, employer-provided coverage is their first interaction with structured healthcare planning.

One of the biggest advantages is accessibility. Individual policies often require medical underwriting, waiting periods, or higher premiums for older applicants. Group insurance removes many of these barriers, allowing employees to access coverage regardless of age or pre-existing conditions in many cases. This makes insurance more inclusive, especially for early-career professionals or employees supporting families.

Another important benefit is predictability during medical events. When employees know hospitalisation costs are covered through group health insurance, they are more likely to seek timely treatment rather than delaying care due to financial concerns. Early treatment often leads to shorter recovery periods and better health outcomes.

Group insurance can also influence long-term financial planning. A group term life insurance policy, for example, provides reassurance that dependents will receive financial support in unforeseen situations. Similarly, group personal accident insurance offers compensation that helps families manage sudden disruptions to income caused by injuries or disabilities.

Modern plans increasingly include preventive care and mental health services, which shift the focus from reactive treatment to ongoing wellbeing. This broader scope reflects how employee expectations around benefits are evolving in India’s workplaces.

Benefits of group insurance for employers

From an organisational perspective, group insurance is not just a cost centre but a strategic investment in workforce stability.

One of the most immediate benefits is stronger employer branding. In competitive hiring markets, candidates often compare benefits packages as closely as salary structures. Companies offering structured group health insurance and life cover signal long-term commitment to employee wellbeing, which can influence acceptance rates during recruitment.

Group insurance also contributes to operational continuity. Employees who have access to healthcare services are more likely to address health issues early, reducing prolonged absences. Accident coverage can provide financial stability during recovery periods, helping employees return to work with fewer financial pressures.

Another important factor is risk management. Instead of providing ad-hoc financial assistance during emergencies, organisations can rely on structured insurance frameworks that distribute risk more effectively. This approach creates predictable budgeting and reduces unexpected financial liabilities.

Additionally, group insurance policies often come with data insights around utilisation patterns, claims trends, and preventive health engagement. Employers can use these insights to refine benefits strategies over time, aligning coverage with the actual needs of their workforce.

Key factors companies consider before buying group insurance

Selecting a group insurance policy requires a balance between employee expectations, budget constraints, and long-term sustainability.

Workforce demographics play a significant role in shaping coverage decisions. Younger teams may prioritise outpatient consultations, mental health support, or fitness benefits, while organisations with a larger proportion of employees with dependents may focus on higher hospitalisation coverage or parent inclusion.

Industry risk exposure also influences policy structure. For example, companies with field operations or travel-heavy roles may prioritise strong personal accident coverage, whereas technology companies may emphasise comprehensive health insurance and preventive care services.

Another critical factor is renewal predictability. Premiums for group health insurance can fluctuate based on claims history and broader healthcare inflation trends. Employers often look for insurers that provide transparency around pricing structures and renewal mechanisms to avoid sudden cost spikes.

Employee experience has become equally important. Ease of claims, clarity of communication, and access to digital tools can significantly affect how employees perceive the value of insurance benefits. Even a comprehensive policy can feel inadequate if the claims process is slow or confusing.

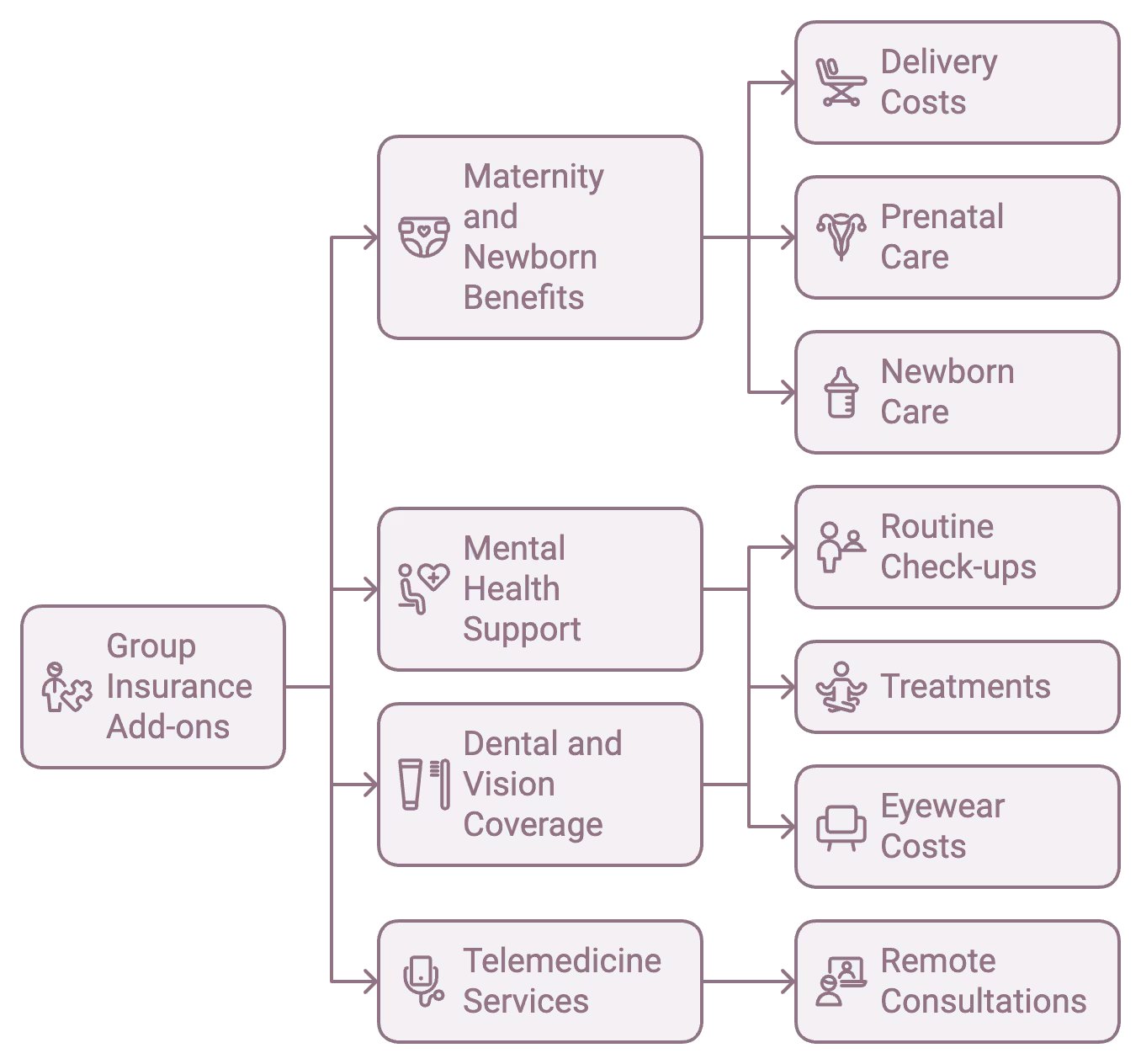

Common features included in modern group insurance plans

Group insurance in India has evolved beyond basic protection. Many policies now include additional benefits designed to support long-term health and engagement.

Some frequently offered features include:

- Preventive health screenings

- Telehealth consultations

- Mental health support programs

- Wellness rewards and fitness tracking integrations

- Coverage extensions for parents or in-laws

These add-ons help organisations shift from reactive healthcare spending to preventive care strategies.

Legal and compliance considerations in India

While group insurance is not mandatory for most organisations, employers often incorporate it into broader compliance and employee welfare strategies.

Companies need to ensure that policy documentation clearly outlines coverage limits, exclusions, and waiting periods. Transparent communication reduces confusion during claims and helps employees understand how to use their benefits effectively.

For organisations offering group term life insurance or accident cover, nominee details and policy records must be maintained accurately. This administrative clarity becomes especially important during claims processing, where delays can create significant stress for families.

Employers also need to align insurance policies with employment contracts and internal HR policies. Clear onboarding communication ensures that employees understand what is covered, whether dependents are included, and how coverage changes during role transitions or exits.

As workplace structures evolve with hybrid and remote work, organisations are increasingly reviewing how accident and health policies apply across different work environments.

How group insurance supports long-term workplace wellbeing

Beyond financial protection, group insurance can influence workplace culture and productivity.

Companies that integrate health insurance with wellness initiatives often see higher utilisation rates and stronger employee engagement. Preventive health programs, for example, encourage employees to monitor health risks early instead of seeking treatment only during emergencies.

This shift toward proactive care is becoming increasingly important as organisations rethink how benefits contribute to long-term business outcomes.

Challenges employers face when implementing group insurance

Despite its advantages, implementing group insurance comes with practical challenges.

Balancing coverage with cost

Employers must manage rising premiums while maintaining meaningful benefits for employees.

Low awareness among employees

Many employees are unsure how to use their insurance effectively, leading to underutilisation.

Renewal pricing fluctuations

Claims history and healthcare inflation can influence pricing during policy renewal cycles.

Addressing these challenges often requires clear communication, employee education, and periodic benefit reviews.

Future trends shaping group insurance in India

The group insurance landscape is undergoing rapid transformation as digital platforms and employee expectations reshape how benefits are delivered.

One major shift is the rise of integrated health ecosystems. Instead of standalone policies, many insurers are bundling teleconsultations, mental health support, preventive diagnostics, and wellness tracking into a unified experience. This integration encourages employees to engage with healthcare proactively rather than only during emergencies.

Another emerging trend is flexible benefits design. Some organisations are experimenting with modular plans that allow employees to choose add-ons such as higher parental coverage or additional accident protection. This approach recognises that a single benefits structure may not suit a diverse workforce.

Technology is also improving transparency around claims and utilisation. Digital dashboards and mobile apps give employees real-time visibility into their coverage, while employers gain insights into overall health trends within the organisation.

As medical inflation and workforce expectations continue to evolve, group insurance is likely to move further toward personalised yet scalable benefit models.

Frequently asked questions about group insurance

What is the difference between group insurance and individual insurance?

Group insurance is purchased by an employer and covers multiple employees under a single policy, while individual insurance is bought directly by a person based on their own needs and risk profile.

Is group health insurance mandatory in India?

Group health insurance is not legally mandatory for most organisations, but many employers offer it as a standard employee benefit.

Can employees keep group insurance after leaving a company?

In most cases, coverage ends when employment ends. Some insurers may offer portability options, but these depend on policy terms.

Which types of group insurance should a company start with?

Many organisations begin with group health insurance and gradually add group term life insurance and group personal accident insurance to create a comprehensive benefits structure.

Group insurance has moved from being a secondary benefit to a central pillar of employee wellbeing in India. Whether through group health insurance, group term life insurance, or group personal accident insurance, companies are increasingly building structured protection systems that support both employees and long-term business resilience.

For organisations evaluating benefits strategies, the goal is not just to offer insurance, but to create a balanced framework that combines protection, preventive care, and financial stability for their teams.